Borrowing

CeFi vs. DeFi Loans: Which is Better?

November 15, 2023

Borrowing

November 15, 2023

Learn the differences between centralized finance (CeFi) and decentralized finance (DeFi) in this short introduction.

Thanks to rapid developments in blockchain technology, the DeFi ("Decentralized Finance") ecosystem has begun offering a wide range of financial services. When it comes to lending and borrowing, decentralized finance lending protocols offer an alternative to traditional financial institutions and even newer firms within centralized finance. For users looking to borrow against digital assets, lending options are generally split up into two categories: DeFi loans and CeFi loans.

DeFi (“Decentralized Finance”) protocols aim to create a more transparent, accessible, and open financial system that does not rely on intermediaries like banks or brokers. Unlike traditional financial institutions, DeFi protocols don't have a centralized authority to manage them.

On the other hand, CeFi loans are facilitated by centralized platforms. CeFi (“Centralized Finance”) platforms also deal with crypto assets, but they operate like traditional financial companies. This means that a private, centralized authority has control over services and user funds.

Each of these approaches has a different set of benefits and drawbacks. In this article, we will discuss both decentralized finance and centralized finance loans in detail, look at their advantages and disadvantages, and examine which options are best suited for different users. CeFi vs. DeFi: Let's get to it!

DeFi loans have garnered significant attention in recent years. Decentralized finance operates entirely through blockchain networks and relies on smart contracts. Smart contracts are programs that represent self-executing agreements which enforce the terms and conditions of financial transactions (such as loans). All DeFi services operate in this way.

Within DeFi, smart contracts enable lenders and borrowers to interact directly without the need for intermediaries or trusted third parties. Lenders can deposit their crypto assets into a lending pool, which is a collection of funds available for borrowing, without trusting any outside entity. Borrowers can then take out loans from the pool by providing collateral. The collateral ensures that the loan is repaid, even if the borrower defaults or the price of the borrowed asset drops.

Since the entire decentralized finance ecosystem is built on blockchain networks, DeFi users cannot use fiat currency. Instead, users must rely on digital assets in the form of cryptocurrencies for all financial transactions. This is in stark contrast to centralized finance where fiat currency is the primary mode of transaction.

The interest rates of DeFi loans are typically determined by supply and demand. They vary according to different factors, such as the type of asset, the loan duration, and the pool's utilization rate. Interest fees are paid by the borrower to the lending protocol which then pays interest to the depositors.

If you're new to DeFi, take a look at "What Can You Do With DeFi Loans" to learn about the uses of DeFi loans, and check out "DeFi Interest Rates: What You Need to Know Before Investing in DeFi" to familiarize yourself with interest rates in DeFi.

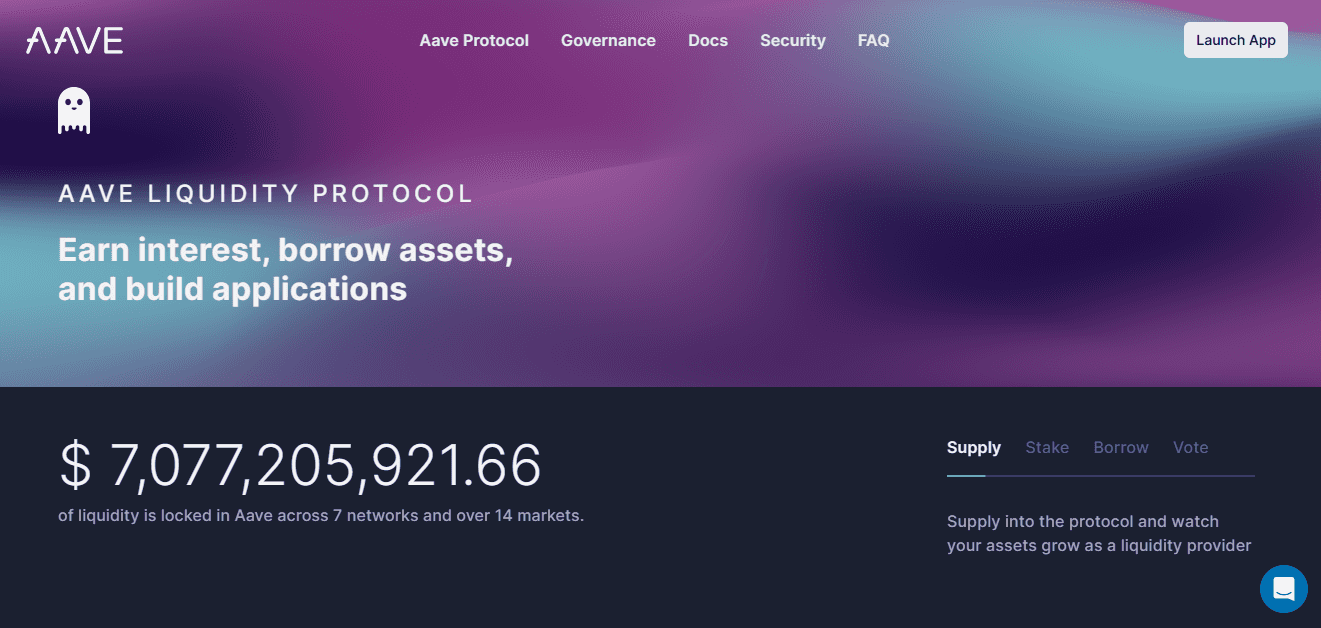

Some examples of DeFi loan platforms include Aave and Compound.

Aave is one of the most prominent open-source, non-custodial DeFi protocols that offers both lending and borrowing platform.

The protocol lets users borrow 20 different cryptocurrencies, including Ether (ETH), Dai (DAI), and U.S. Dollar Coin (USDC).

Aave offers several features that make it stand out from other DeFi loan platforms, such as flash loans, rate switching, and collateral swapping. Aave also has its own governance token, AAVE, which gives holders the right to vote on protocol changes and earn rewards.

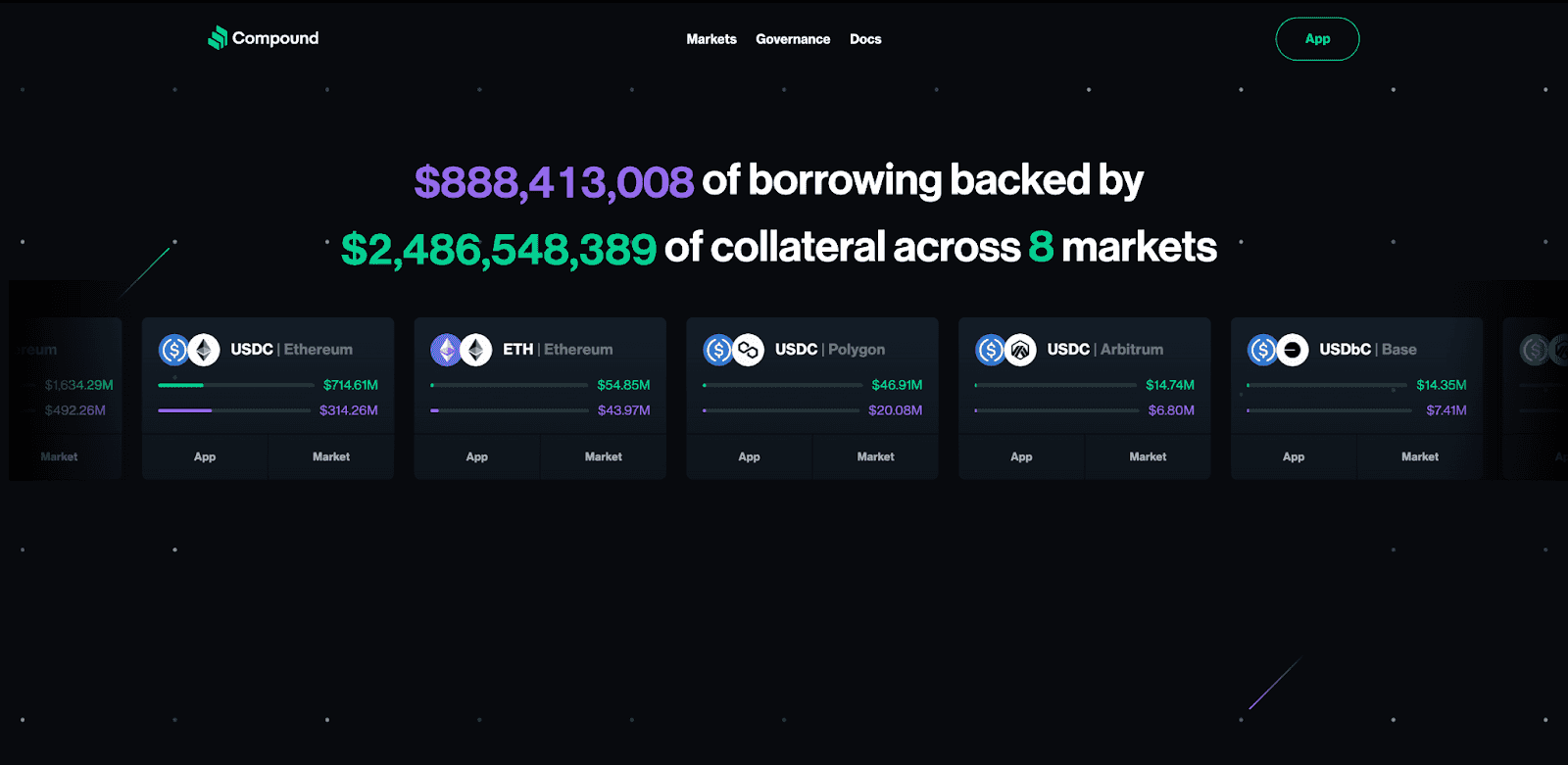

Compound is another popular DeFi protocol.

It functions similarly to Aave and comes with several unique features. Compound uses an algorithmic interest rate model which automatically adjusts interest rates based on the supply and demand for assets within the platform. This dynamic system ensures competitive and efficient interest rates for both lenders and borrowers.

Compound supports borrowing of USDC and ETH and lending of seven cryptocurrencies including ETH, Uniswap (UNI), Chainlink (LINK), and others. Compound also has a governance token called COMP, which gives users the right to propose and vote on changes to the protocol. (https://www.gemini.com/cryptopedia/what-is-compound-and-how-does-it-work#section-earn-interest-with-compound-lending)

To learn more about Compound and Aave, check out our review of both platforms.

DeFi loans have a number of benefits, including:

Competitive Interest Rates: One of the most attractive features of DeFi loans is the potential for significantly lower interest rates than traditional CeFi loans. These rates are not set by a centralized authority like the Federal Reserve but are determined by the market's supply and demand dynamics.

Transparency: DeFi protocols are often praised for their transparency. Users can trace every transaction on the blockchain, ensuring there are no hidden fees, interest rate manipulations, or unexpected changes. Most DeFi lending platforms also don’t allow pledged collateral to be re-lent, which is a risky practice known as rehypothecation. This transparency provides a level of trust that isn't usually present in centralized systems.

Non-Custodial: When users borrow or lend through a DeFi platform, they retain ownership of their assets. These assets are not entrusted to a centralized entity, reducing the risk associated with traditional financial institutions.

Flexibility: DeFi platforms typically support a wide range of cryptocurrencies and tokens as collateral. Some DeFi platforms even allow borrowers to create their own synthetic assets or use non-fungible tokens (NFTs) as collateral. This flexibility allows users to put a diverse portfolio of assets to work securing loans. In contrast, centralized platforms usually limit the types of collateral they are willing to accept.

Available worldwide: Anyone with an internet connection and a crypto wallet can take out a DeFi loan, regardless of their location, identity, or credit history.

While DeFi loans have many benefits, there are also some downsides:

Complexity: DeFi platforms can be challenging to use, especially for newcomers. To take out a DeFi loan, users need to connect a compatible wallet, navigate the platform's interface, have some knowledge of smart contracts, and understand how to withdraw funds. The learning curve can be steep.

Smart-Contract Risk: Since DeFi protocols operate strictly based on their software code, any bug, flaw in the code, or malicious design can lead to protocol failure, or allow malicious actors to steal funds held inside the smart contracts. While many DeFi protocols undergo extensive auditing to reduce the likelihood of a potential exploit, there is no guaranteed method to fully eliminate this risk. Users should research DeFi protocols that they intend to use exetensively so they can better understand the risks.

Difficulty in Loan Tracking: DeFi platforms may not provide convenient features like collateral alerts or intuitive interfaces for tracking loan status. This means that borrowers must actively manage and monitor their loans, which can be cumbersome.

Lack of Customer Support: DeFi operates in a decentralized environment, and while this provides many benefits, it also means that there is no centralized customer support to assist with the lending process. Users are entirely responsible for their funds and must troubleshoot issues independently.

DeFi loans offer many advantages for those who want more transparency, control, and flexibility over their loans. Despite some challenges stemming from the independent and permissionless nature of DeFi, these types of loans are a popular choice for users looking for the best loan rates. For those comfortable with the intricacies of DeFi, DeFi loans can be an excellent choice to get liquidity without selling crypto assets.

In the following section we will explore CeFi loans, providing a comprehensive breakdown of their advantages and disadvantages.

CeFi loans, or loans from centralized finance lenders, are a type of loan that is issued and managed through centralized platforms. Centralized platforms are intermediaries or lenders that facilitate lending and borrowing (or other banking services) while also applying their own rules and abiding by all financial regulations. Generally, this is thought of as traditional finance. However, offering crypto-backed loans is not very common for traditional financial services, so specialized companies offer these loans to users interested in cryptocurrencies.

CeFi loans work through a custodial model, which means that users have to deposit their crypto assets into the platform’s blockchain wallet and trust the platform to secure and manage their funds. Some platforms won't move these assets until you repay your loan while others will rehypothecate them to earn extra yield, which can be dangerous in the event of a market crash.

In CeFi, loan interest rates are up to the platform’s discretion but usually include the platform adding a margin to a benchmark rate such as the Fed prime rate. This usually means that interest rates for CeFi loans will go up or down along with the rates set by central banks. Many CeFi platforms charge fees for their services include origination, withdrawal, and platform fees, adding to the borrowing costs.

One popular CeFi platform is Nexo.

Based out of Switzerland, Nexo is one of the largest CeFi crypto lending platforms in the world. Nexo lets you borrow money using your crypto assets as collateral. You can choose from over 40 supported cryptocurrencies and get cash or stablecoin. However, Nexo is not available in all countries.

Some of the benefits of centralized loans are:

Ease of use: One of the most notable advantages of CeFi lending platforms is their user-friendly approach. These platforms are designed to simplify the lending process, making it accessible to a broader audience. Borrowers typically don't need to connect wallets, understand complex smart contracts, or navigate intricate blockchain interfaces.

Take out loans in fiat: One of the major benefits of centralized loans is that users can take out loans in fiat currencies like USD or EUR against their crypto collateral. This allows users to access liquidity without selling their crypto assets. However, CeFi platforms are not the only way to take out US dollars against crypto collateral.

Loan dashboards: CeFi lending platforms often provide users with intuitive dashboards and notifications to keep them informed about the status of their loans.

Some of the downsides of centralized loans are:

Lack of Transparency: A critical drawback of CeFi loans is the lack of transparency. These platforms are not as transparent as DeFi protocols, so users have limited insight into how the platform is utilizing their funds. In some unfortunate cases, CeFi platforms have faced insolvency issues, resulting in the loss of customer funds. This absence of transparency can lead to platform-related risks.

High Annual Percentage Rates (APRs): CeFi loans often come with high interest rates, especially when compared to DeFi alternatives. The cost of borrowing can be steep, as these platforms take a more traditional lending approach which requires them to generate significant revenue to cover their operating costs, leading to higher APRs.

Limited Supported Assets: Unlike DeFi, where the range of supported assets is extensive and quickly expanding, CeFi platforms tend to be more selective in terms of the cryptocurrencies they accept as collateral. This may limit the options borrowers have, especially if they hold less mainstream or newer cryptocurrencies.

Centralized loans offer a lot of convenience and simplicity for users who want to access fiat liquidity or use various services from one platform. However, they also come with many downsides and uncertainties that users should be mindful of.

Now that we've examined the features and tradeoffs of both DeFi and CeFi loans, this begs the question: which one is better? DeFi or CeFi?

When it comes to DeFi vs. CeFi, the better type of loan depends on your individual preferences and needs. If you want lower fees, self-custody, and more flexibility, decentralized finance may be a good option. If you want something more traditional, centralized finance may be for you.

However, if you want to get the benefits of both, you should take a look at Rocko. With Rocko, you can get the convenience and simplicity of CeFi but the security and low interest rates of DeFi.

Rocko is a new platform that enables crypto owners to easily and securely borrow from popular DeFi protocols like Aave, Compound, and Morpho and get funds in minutes — no experience needed! Use the loan to purchase real estate, pay down higher-rate debt, make everyday purchases, and much more.

Rocko also provides a loan management dashboard and tools like text and email alerts to help manage your loan and collateral. The Rocko team consists of experienced crypto enthusiasts who are ready to help you with any questions you may have. You can join the Rocko Discord server, follow our Twitter account, or visit our resource center to learn more about DeFi borrowing.

Sign up for Rocko and get a loan today!

Rocko does not guarantee the reliability of the Site content and shall not be held liable for any errors, omissions, or inaccuracies. The opinions and views expressed in any articles on rocko.co are solely those of the author(s) and do not reflect the opinions of Rocko. The information provided on the Site is for informational purposes only, and it does not constitute an endorsement of any of the products and services discussed or investment, financial, or trading advice. A qualified professional should be consulted prior to making financial decisions.

Crypto & DeFi

Why Borrow Against Staked ETH? Liquid-staking tokens (LSTs) such as stETH, wstETH, cbETH and rETH let you keep earning staking rewards while…

June 17, 2025

Crypto & DeFi

Bitcoin Mining Loans: How to Fund Your Mining Business Bitcoin mining is the backbone of the Bitcoin network—a decentralized process where…

May 07, 2025

Crypto & DeFi

The 5 Best Solana Loan Platforms of 2025 As Solana cements its position as a leading blockchain for high-speed, low-cost DeFi applications…

May 06, 2025